The Wheel Is Turning

What an obscure investing framework tells us about the best time to sell a creator economy business

There is a framework that institutional investors use to time capital deployment into entire industries. It’s called the capital cycle. Marathon Asset Management built one of the most respected long-only funds in the world using it. The insight is simple: the best time to buy into an industry is when everyone else has given up on it. The best time to sell is when supply is constrained and strategic buyers are competing for assets.

The creator economy just finished three of the four stages. This isn't true for the entire space. New agencies still launch every day. But for the established, profitable tier, the cycle looks exactly like this.

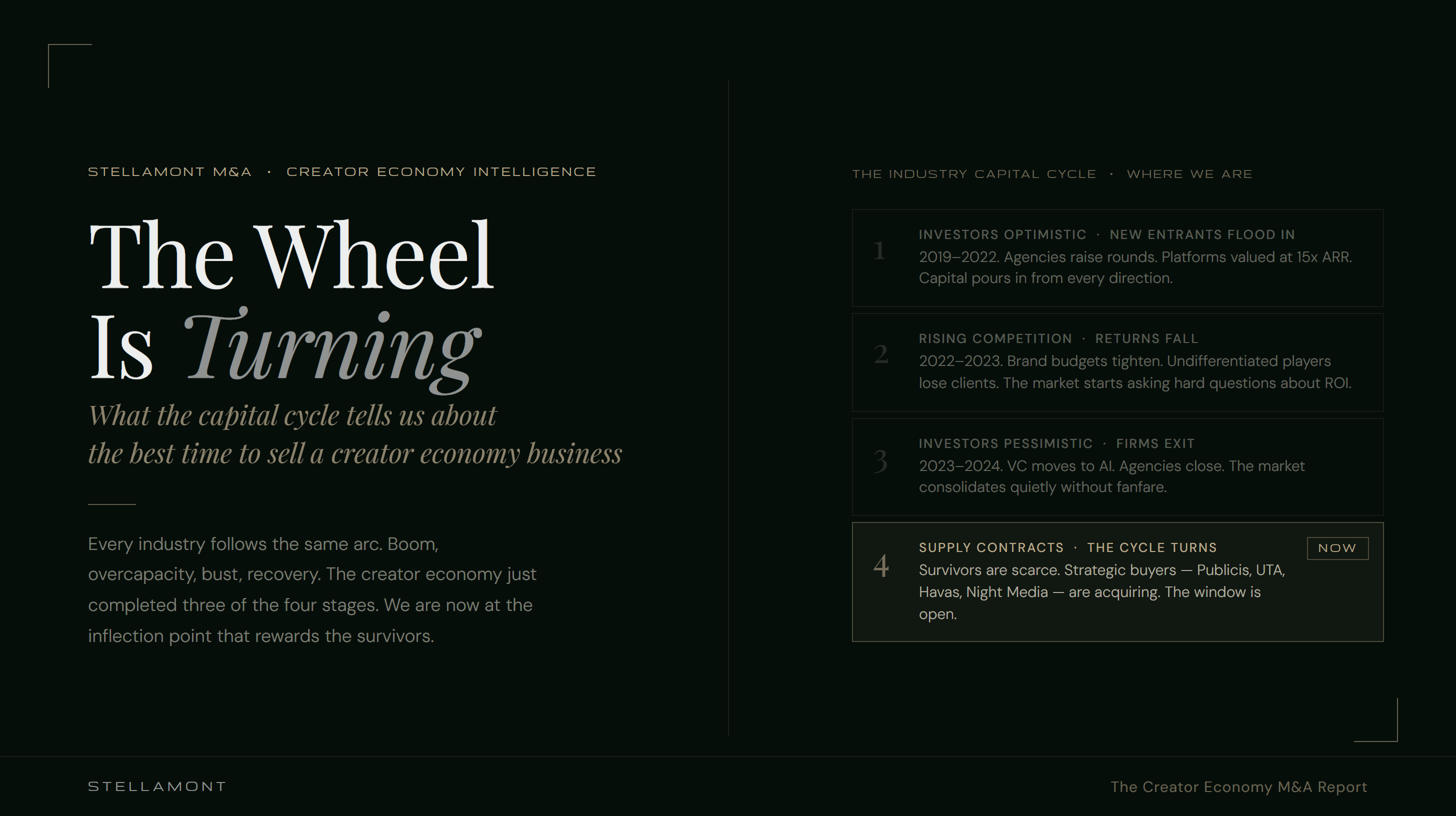

The Cycle

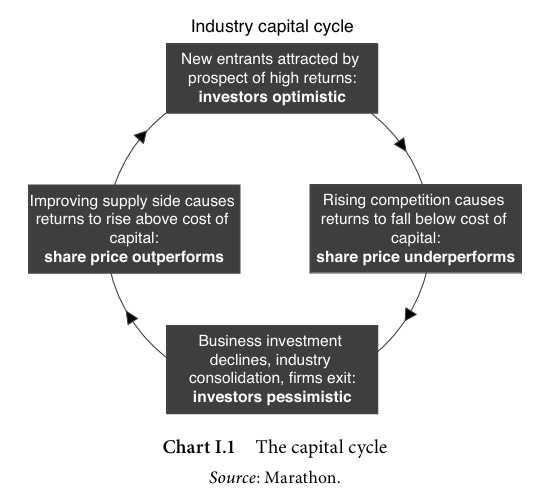

Marathon’s framework breaks every industry into four phases:

Stage 1 — Investors Optimistic / New Entrants Flood In

Capital chases narrative. Everyone wants a piece of the opportunity. New firms launch, platforms raise at impossible multiples, and money enters faster than the market can absorb it.

For the creator economy, this was 2019 to 2022. Influencer marketing agencies raised rounds. Creator platforms were valued at 15x ARR. SPACs targeted UGC businesses. The pitch was simple: the internet is eating advertising, and these agencies own the relationships.

Stage 2 — Rising Competition / Returns Fall

Supply exceeds demand. Undifferentiated players compete on price. Clients get more selective. The firms that grew fast on the promise of scale start losing accounts.

This hit between 2022 and 2023. Brand performance budgets tightened as inflation rose. Agencies that couldn’t prove ROI lost retainers. The market started asking hard questions that the optimistic phase never had to answer.

Stage 3 — Investors Pessimistic / Firms Exit

Capital retreats. The narrative dies. VC moves to the next thing. Weaker operators close. Consolidation happens quietly, without fanfare, because nobody is writing about this sector anymore.

This was 2023 and 2024. Venture moved to AI. Mid-tier influencer agencies contracted or shut down. The firms that survived were leaner, more defensible, and running on real economics.

Stage 4 — Supply Contracts / The Cycle Turns

This is where we are now.

Marathon’s observation, backed by decades of equity research, is that the highest returns come not from chasing what is popular but from buying what has been abandoned and is now scarce.

The same logic applies to sell-side timing in M&A.

When an industry is in Stage 1, buyers overpay because they are competing on optimism. When it hits Stage 3, buyers pull back because the narrative is broken. But Stage 4 is different. Supply is contracted. The survivors are proven. And strategic buyers who missed the window in Stage 1 are now under pressure to acquire rather than build.

That is exactly the setup in the creator economy right now.

Publicis acquired Influential. UTA expanded its creator division. Havas is active. Night Media is acquiring. The buyers who sat out 2021 and 2022 because valuations were irrational are now moving -- because the assets that remain are worth acquiring and the price of waiting keeps going up.

What This Means If You Own One of These Businesses

If you built a creator economy business and survived the last three years, you are not just still standing. You are scarce. That scarcity has value -- but only if you move while the strategic window is open.

Capital cycles do not wait. Stage 4 does not last forever. The firms that sell into buyer competition extract significantly more value than the ones that wait until the next optimistic phase drives the narrative back up.

The question is not whether the market for your business exists. It does. The question is whether you are positioned to access it before the window closes.

✦ Talk to Stellamont

Stellamont advises founders of creator economy businesses on sell-side M&A. If you are thinking about a process in the next 12 to 18 months, reach out at ruben@stellamont.com.