The Creator Economy Is Growing. That Doesn't Mean Your Business Is Sellable.

Capital is flowing into creator-led media, talent, agencies, and infrastructure. But buyers are drawing a sharper line between businesses that participate in the market and businesses that can survive

Traditional entertainment is contracting while creator advertising and M&A continue to grow. The apparent contradiction disappears once you understand what buyers are actually acquiring.

A founder recently described what the last several years had done to her entertainment business.

Clients had left, most of the staff was gone, and domestic film and television production had slowed dramatically. New business was becoming harder to win, while the clients who remained were on month-to-month agreements and could leave at any time.

Her experience raises an uncomfortable question:

If the creator economy is growing, why are some entertainment and talent businesses struggling?

The answer is that “entertainment,” “media,” and “the creator economy” are not one market moving in one direction.

Traditional production is contracting while creator advertising continues to expand. M&A remains active, but buyers are becoming much more selective about the difference between a growing category and a transferable company.

That distinction matters for every founder considering a sale.

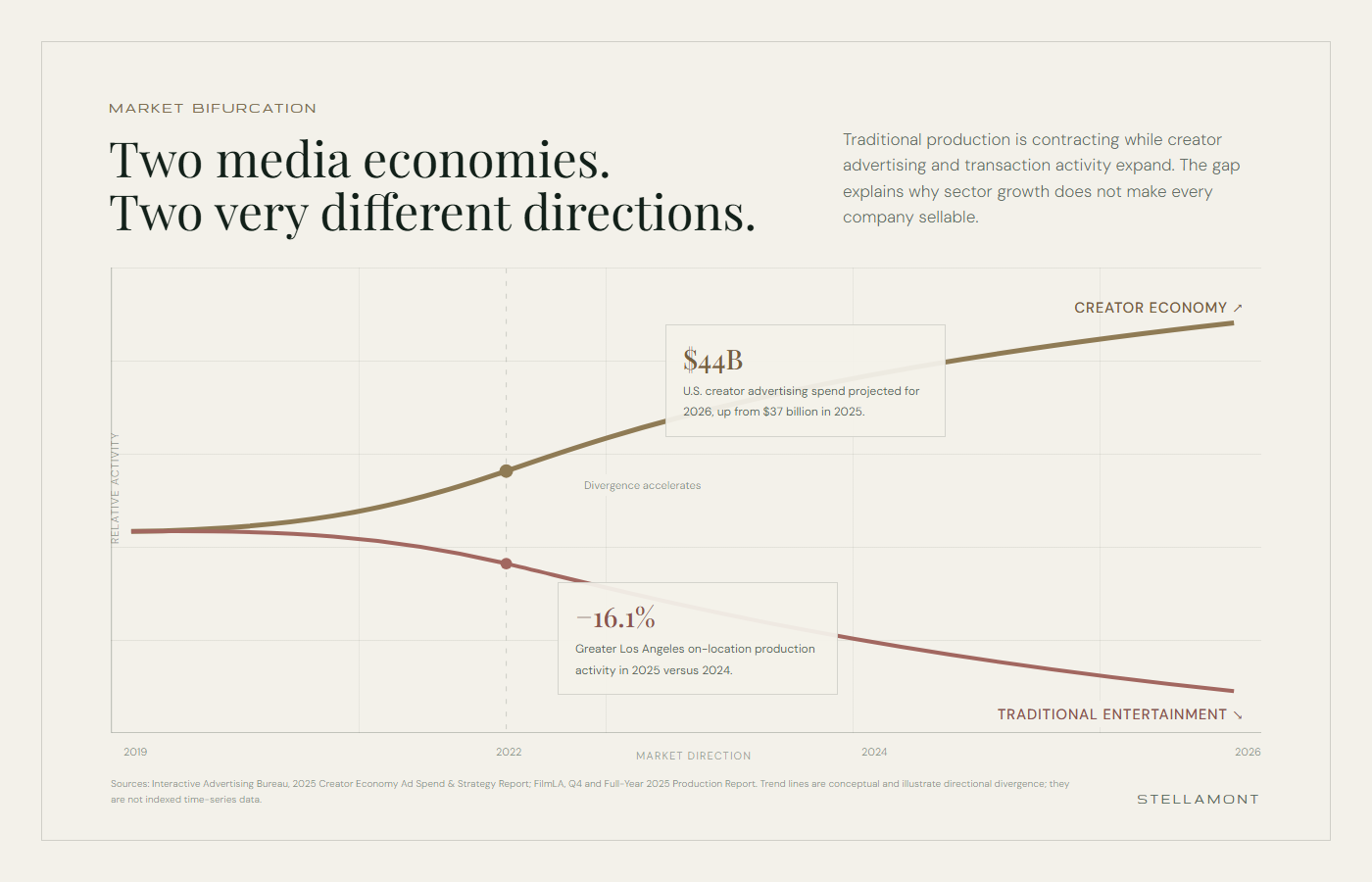

Two media economies are moving in opposite directions

The divergence is visible in both operating and advertising data.

Traditional production and creator advertising are moving in opposite directions. Sources: IAB and FilmLA; trend lines are conceptual rather than indexed time series.

The pressure on traditional entertainment is real.

FilmLA reported that Greater Los Angeles on-location production fell 16.1% in 2025 compared with 2024. Feature-film activity ended the year 31.7% below its five-year average.

Fewer productions mean fewer launches, fewer working actors, fewer publicity campaigns, and less spending across the network of firms that historically served Hollywood.

For a business whose revenue depends on domestic film and television production, this is not a temporary headline. It is an operating reality.

At the same time, creator-led advertising is moving in the other direction.

According to the Interactive Advertising Bureau, U.S. creator advertising spend was projected to reach $37 billion in 2025, an increase of 26% year over year and nearly four times the growth rate of the broader media industry. IAB expects the figure to approach $44 billion in 2026. Nearly half of creator-ad buyers now consider creators a “must buy.”

The creator economy is not insulated from economic pressure. It is taking share from traditional media because brands increasingly see creators as a measurable distribution channel.

That money tends to reward businesses connected to:

Influencer and creator campaigns

Social-first creative

Athlete and talent partnerships

Performance marketing

Affiliate and social commerce

Owned audiences and intellectual property

Audience data, attribution, and measurement

Recurring brand relationships

It does not automatically reach every company with an entertainment logo or celebrity client list.

M&A is active but activity is not immunity

The same distinction appears in the transaction market.

Public-relations M&A slowed in 2025, with PRovoke Media and Davis+Gilbert identifying 80 transactions, down from 99 in 2024. Buyers increasingly favored integrated firms with differentiated capabilities, technology, analytics, healthcare exposure, and meaningful scale.

Activity then accelerated in the first half of 2026. Davis+Gilbert reported 44 completed PR and earned-media transactions, with more than 60% of sellers generating less than $6 million in revenue. Influencer and celebrity partnerships moved higher on buyers’ priority lists. Reputation and crisis management, data analytics, and content strategy remained in demand.

Creator-economy M&A has also remained active across agencies, talent management, media, software, commerce, and infrastructure.

But this does not mean buyers will acquire any business that operates in the category.

Instead, buyers are underwriting creator companies the same way they underwrite every other company:

• Is revenue growing?

• Is it recurring?

• Is it contractually durable?

• Is the customer or talent base concentrated?

• Are margins healthy?

• Can the business operate without the founder?

• Do the relationships transfer after a change of control?

• Is there a system behind the revenue—or only an individual?

The market may be growing while a particular company remains difficult to sell.

A category is not an asset

Consider three anonymized businesses.

The first is a traditional entertainment publicity boutique. It has recognizable clients and decades of relationships, but revenue has declined, the team has contracted, clients are month-to-month, and nearly every important relationship belongs to the founder.

The second represents athletes and digital creators, executes brand partnerships, has grown rapidly, and has signed revenue scheduled through the remainder of the year. It still faces concentration and founder-dependence risk, but buyers can see financial momentum and strategic scarcity.

The third represents a carefully curated roster of digital creators in attractive, brand-friendly consumer categories. Its niche aligns with consumer-brand spending, and the roster may support multi-creator campaigns, affiliate revenue, commerce, and owned products. But without financial statements, creator-level concentration, contract terms, and retention history, its strategic appeal remains a hypothesis rather than an underwritable transaction.

All three can be described as entertainment or creator-adjacent businesses.

Only the underlying evidence determines whether they are sellable.

Month-to-month revenue is not automatically worthless

Founders often assume that recurring billing equals recurring revenue.

Buyers make a finer distinction.

A monthly retainer that can be canceled tomorrow is not equivalent to a multi-year agreement. But contract duration is not the only evidence of durability.

A client that has renewed every month for eight years may demonstrate stronger behavioral retention than a newly signed one-year contract.

Buyers evaluate durability using multiple factors, including:

Contract term and cancellation rights

Historical client or talent tenure

Gross and net revenue retention

Churn by year

Reason for each material departure

Revenue concentration

Relationship ownership inside the team

Performance through previous market cycles

Month-to-month relationships become a valuation problem when they are combined with declining revenue, high concentration, and founder dependence.

The founder-dependence discount

Many service businesses begin because the founder is exceptional at the work.

That strength becomes a transaction risk when the founder remains the only reason clients stay.

If every client calls the founder, every employee relies on the founder, and every new engagement comes through the founder’s reputation, a buyer is not acquiring an autonomous company. The buyer is acquiring a relationship book plus the founder’s continued labor.

Those transactions can still happen, but the structure changes.

Instead of receiving the full price at closing, the founder may receive:

A smaller upfront payment

An earnout tied to retained revenue or gross profit

A multi-year employment agreement

Equity in the acquiring platform

Additional payments as relationships transfer

This is why two firms with identical EBITDA can receive very different offers.

One has a leadership team, durable agreements, diversified revenue, and repeatable systems. The other has a talented founder and a collection of relationships that may disappear when the founder leaves.

What buyers are paying for now

Across creator, talent, media, and communications transactions, the premium attributes are becoming clearer.

1. Revenue engines, not audience narratives

Follower counts and recognizable names can open a buyer’s door. They do not complete diligence.

Buyers want evidence that attention converts into recurring revenue, commerce, licensing, subscriptions, brand partnerships, or owned intellectual property.

2. Diversified talent and clients

One creator, athlete, or client contributing a disproportionate share of income can materially reduce value. If that relationship leaves, the buyer’s investment thesis may disappear overnight.

3. Transferable contracts and relationships

The agreement must survive a transaction—or the person represented must be willing to affirmatively remain. Buyers will examine assignment clauses, change-of-control provisions, exclusivity, termination rights, and historical churn.

4. Leadership beneath the founder

Managers must own meaningful relationships. Finance must produce reliable information. Sales must originate opportunities without the founder. Operations must function through documented processes.

5. Data and measurement

Brands increasingly expect measurable outcomes. Agencies with audience intelligence, attribution, campaign analytics, and repeatable reporting are more valuable than firms relying only on personal judgment and access.

6. Profitable growth

The creator label does not excuse weak economics. Buyers still want healthy margins, controlled working capital, clean revenue recognition, and confidence that growth will not require expenses to rise at the same rate.

A founder’s sellability test

Before launching a transaction, a founder should be able to answer the following questions:

What percentage of revenue is truly recurring?

How much revenue comes from the largest client or creator? The top five?

How long have the most important relationships stayed?

Can contracts be assigned after a change of control?

Who owns each relationship besides the founder?

What has annual churn looked like for the last three years?

Can the company add meaningful revenue without doubling headcount?

Are gross billings and net agency revenue clearly separated?

What is adjusted EBITDA after paying the founder a market salary?

How long is the founder genuinely willing to remain after closing?

If those questions cannot be answered, the business may still have strategic potential. It is simply not ready for market.

The creator economy is growing up

The creator economy’s maturation is good news for founders—but maturity brings discipline.

Buyers are no longer paying simply for proximity to creators. They are paying for scalable systems, durable economics, proprietary access, differentiated capabilities, and companies that can survive a transition of ownership.

The opportunity is real. So is the divide.

Traditional entertainment businesses exposed to declining production may need to reposition toward creators, brands, reputation management, digital distribution, or measurable campaign services. Creator-native firms may need to reduce concentration, strengthen contracts, build leadership, and document recurring revenue before approaching buyers.

The strongest transaction story is not:

“We operate in the creator economy.”

It is:

“We built a durable revenue engine inside one of media’s fastest-growing channels—and that engine will continue after the founder steps back.”

That is what buyers are competing to own.

Sources

FilmLA — Q4 and Full-Year 2025 Production Report

Interactive Advertising Bureau — 2025 Creator Economy Ad Spend & Strategy Report

Davis+Gilbert — Mid-Year 2026 PR M&A Tracker

PRovoke Media — 2025 M&A Review

✦ Talk to Stellamont

Thinking about selling your agency, talent management firm, creator business, or media company? We advise founders on valuation, transaction preparation, and competitive sell-side processes across the creator economy.